Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Why Industry Context Drives Credibility in Climate and Sustainability Disclosures?

As global sustainability and climate disclosure frameworks converge around investor-grade transparency, organisations face mounting pressure to publish credible, comparable, and decision-useful reports. But beneath the surface of GRI checklists and ISSB content indices lies a foundational truth: materiality is never generic. It is—and must be—industry-specific, operationally grounded, and systemically integrated.

This article explores why understanding sector context is essential to credible reporting, drawing a sharp contrast between two industries at opposite ends of the ESG risk spectrum: construction and advanced technology. Using real-world scenarios, systems-thinking, and clause-level references to GRI 2021 Standards and IFRS S1/S2 by the International Sustainability Standards Board (ISSB), we argue for a calibrated approach to materiality, climate risk mapping, and assurance.

Materiality is Industry-Defined, Not Framework-Imposed

GRI vs ISSB: What’s the Difference?

- GRI Standards adopt a double materiality perspective: what impact an organization has on the environment, people, and society.

- ISSB’s IFRS S1 and S2 adopt an enterprise value perspective: what sustainability-related risks and opportunities affect the company’s ability to generate cash flows over time.

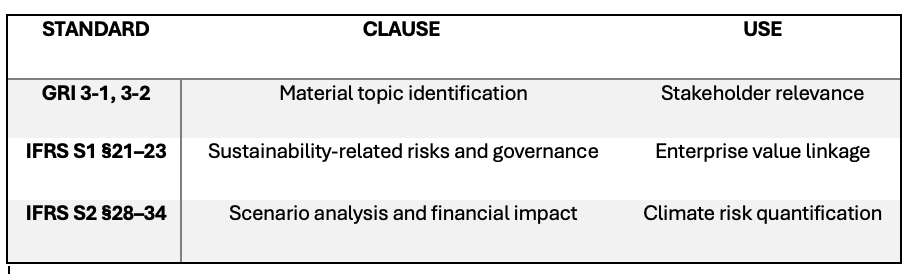

GRI 3-1 and 3-2: require the organisation to determine material topics through stakeholder input and sustainability context.

Link to GRI 3 Standard

IFRS S1 §21–22 and S2 §24–27: require organisations to disclose significant sustainability-related risks and opportunities that could reasonably be expected to affect enterprise value.

IFRS S1

IFRS S2

Key Takeaway:

Materiality is not static—and it certainly isn’t uniform across sectors. Industry context defines what is truly material, how it evolves, and how it must be disclosed.

Why Business Operations Shape Material Risk

Materiality must be viewed through the lens of the organisation's value chain, business model, and operating realities. Let’s compare:

Construction Industry: Tangible, Site-Based Risks

- Typical Material Issues (GRI):

- GHG emissions (GRI 305), Water use (GRI 303), Waste (GRI 306), Health & Safety (GRI 403), Procurement practices (GRI 308).

- Enterprise Value Risks (IFRS S2):

- Physical climate risks (e.g., flooding, heat stress), carbon taxes on materials, delays from extreme weather.

Example:

A construction company building metro tunnels in coastal cities must disclose under IFRS S2 28–34 how extreme rainfall disrupts timelines, inflates insurance premiums, and impacts project financials—far beyond what a GRI-only emission report can reveal.

Advanced Tech Industry: Intangible, Systemic Risks

- Typical Material Issues (GRI):

- Data Privacy (GRI 418), Governance (GRI 205), Workforce Diversity (GRI 405), Energy Use (GRI 302), Innovation (GRI 201).

- Enterprise Value Risks (IFRS S1/S2):

- Regulatory transition risks (AI ethics, carbon pricing), Scope 2 emissions from compute, IP litigation, cloud resilience.

Example:

A generative AI firm with data centres across regions must disclose under IFRS S1 24 and IFRS S2 29 how Scope 2 costs and policy bans on high-energy models could reduce operating margins, increase capital costs, and alter access to key markets.

Systems Thinking: Mapping Materiality to Enterprise Risk

Understanding the interdependencies within an organisation—between ESG risks, financial controls, governance structures, and decision-making—is essential for meaningful disclosure.

Construction System View

- Inputs: Carbon-intensive materials, on-site energy use, labor practices.

- Processes: Engineering, project delivery, compliance management.

- Outputs: Infrastructure assets, community impact, climate exposure.

Systems risk example: A delay from climate-induced flooding doesn’t just affect a single project—it disrupts revenue recognition, triggers liquidated damages, and escalates financing costs across the portfolio.

Advanced Tech System View

- Inputs: Data, intellectual property, cloud energy.

- Processes: Algorithm development, data hosting, compliance.

- Outputs: Software services, digital risk exposure, investor scrutiny.

Systems risk example: A data breach leads not only to reputation loss, but also to regulatory fines (GDPR), increased security spend, and downgraded ESG ratings that affect cost of capital.

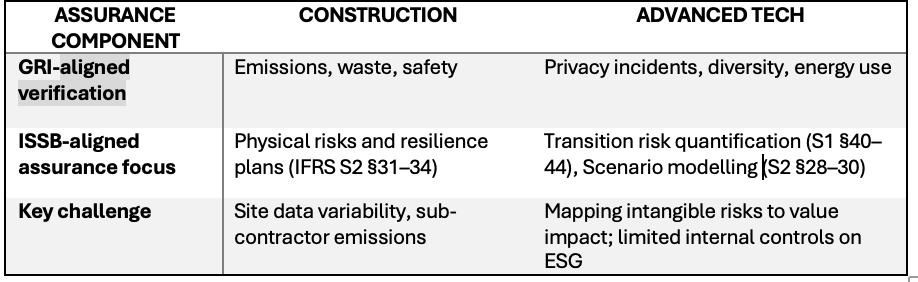

The Assurance Challenge: What Gets Verified Must First Be Valued

Without sector-specific scoping, assurance becomes generic—or worse, misleading. Here's how sector affects assurance strategy:

The Real Risk of Generic Reporting

Failing to tailor materiality by industry leads to:

- Irrelevant disclosures that don’t reflect what matters to investors or stakeholders.

- Inconsistent assurance outcomes, limiting report credibility.

- Compliance risk, especially under evolving global mandates (e.g., CSRD, SEC Climate Rules).

- Lost opportunity to build trust and unlock ESG-linked capital.

Industry context is the cornerstone of credibility

Materiality is not a box-ticking exercise—it is a strategic compass. To meet both stakeholder expectations (GRI) and investor requirements (ISSB), companies must move beyond boilerplate ESG disclosures and ground their reports in operational, financial, and sectoral realities.

Construction firms must focus on physical risk, emissions from materials, and resilience of built assets.

Tech companies must prioritise data ethics, energy cost modelling, and regulatory transition risks.

Recommended Actions

- Revisit your materiality process: Apply a dual-lens filter using GRI and ISSB to segregate impact and enterprise risks.

- Engage operations and finance teams early: Materiality cannot be ESG’s burden alone.

- Use the right clauses to structure reporting and assurance:

- Align materiality to risk registers, CAPEX plans, and board oversight—not just stakeholder interviews.

The Bottom Line:

Materiality without industry context is noise. But with it, ESG reporting becomes a narrative of relevance, resilience, and readiness.

Author: Bitasta Roy Mehta, Founder - Scope3Nexus Consulting Pte Ltd

Disclaimer: This article is intended for informational purposes only. Its primary aim is to highlight the importance of understanding sector-specific differences in sustainability reporting and how these distinctions can inform effective report development. Readers seeking regulatory compliance should refer directly to the official GRI Standards and ISSB’s IFRS S1 and S2, in accordance with their country- and sector-specific disclosure requirements.